Understanding the Recent Gold Rally and Currency Concerns

Gold has surged more than 60% this year, climbing above $4,300 per ounce, while numerous other asset classes have also achieved record highs. This remarkable advance has generated significant attention and raised questions among investors about whether this episode differs from previous rallies.

The phenomenon has been labeled the “debasement trade,” reflecting concerns that governments may be incentivized to diminish currency strength through expansive fiscal policies and supportive monetary measures. These factors, combined with a softer dollar, have driven some market participants toward assets such as gold that are perceived as reliable stores of value, particularly amid renewed stock market turbulence.

Although fiscal deficit concerns are warranted, historical evidence demonstrates that forecasting gold’s trajectory is challenging, and multiple factors beyond monetary policy and exchange rates are fueling broader market gains. For investors with long time horizons, the question is not whether to choose between equities and bonds versus gold, but rather determining the appropriate allocation to each within a diversified portfolio.

Most crucially, distinguishing between short-term trading opportunities and long-term financial objectives—such as generating income and building wealth—becomes especially important after an asset has already experienced substantial appreciation.

Understanding currency debasement through history

Although currency debasement has existed for millennia, concerns about this practice tend to reemerge periodically. Traditionally, “debasement” described the practice of governments decreasing the precious metal content in coinage. This technique enabled authorities to produce additional coins from identical quantities of precious metals, though it simultaneously diminished each coin’s purchasing power.

Contemporary currencies are predominantly “fiat currencies,” deriving their worth from confidence in issuing governments rather than precious metal backing. Consequently, modern debasement concerns focus on whether governments might tolerate elevated inflation and currency depreciation, as these conditions would ease the burden of servicing outstanding debt obligations.

These concepts connect to theories that gained traction following the 2008 financial crisis. Economists Reinhart and Rogoff identified what they termed “financial repression”—policies maintaining artificially suppressed interest rates to diminish government debt’s real burden. Such policies penalize savers, as cash holdings lose value when interest rates fail to match inflation. Given ongoing national debt expansion, investor anxiety about these dynamics and subsequent interest in value-preserving assets is understandable.

Despite these long-term considerations, current evidence regarding whether debasement is actually occurring remains mixed. Inflation measures have proven persistent but not extreme—the Consumer Price Index, Personal Consumption Expenditures Index, and Producer Price Index all register at 3% or below. Additionally, bond markets are not anticipating elevated inflation levels. The 10-year Treasury yield has recently declined to approximately 4% or less, while Treasury Inflation-Protected Securities (TIPS) imply an inflation expectation of just 2.3%.

Two additional considerations merit attention. Global central banks have accelerated gold purchases to strengthen reserve positions, driven by geopolitical tensions and dollar weakness. Furthermore, although the dollar has depreciated roughly 10% this year, it remains near the upper end of its two-decade range, indicating continued relative strength from a historical perspective.

Forecasting gold rallies presents significant challenges

Given gold’s speculative nature, investor fascination with the metal is understandable. Throughout recent decades, gold has experienced dramatic surges with varying outcomes. During the late 1970s, gold soared amid stagflation fears and questions about Federal Reserve independence. Prices peaked above $800 in 1980—a threshold not revisited until 2007.

A comparable pattern emerged following the 2008 financial crisis as central banks implemented massive stimulus programs. Many investors reasonably feared runaway inflation and dollar collapse, yet neither materialized. Gold doubled between 2009 and 2011, reaching approximately $1,900 per ounce, before retreating toward $1,000 in subsequent years. This decline occurred despite the Fed not beginning to taper stimulus until 2013 or lifting rates from zero until 2015.

The accompanying chart illustrates gold’s performance relative to the S&P 500 since the 2007 market peak. Although gold has delivered strong returns during certain periods, providing diversification advantages, the S&P 500 has generated superior returns across the entire timeframe. For those fixated on daily market fluctuations, this outcome may seem unexpected, underscoring the importance of evaluating all asset classes through a portfolio lens.

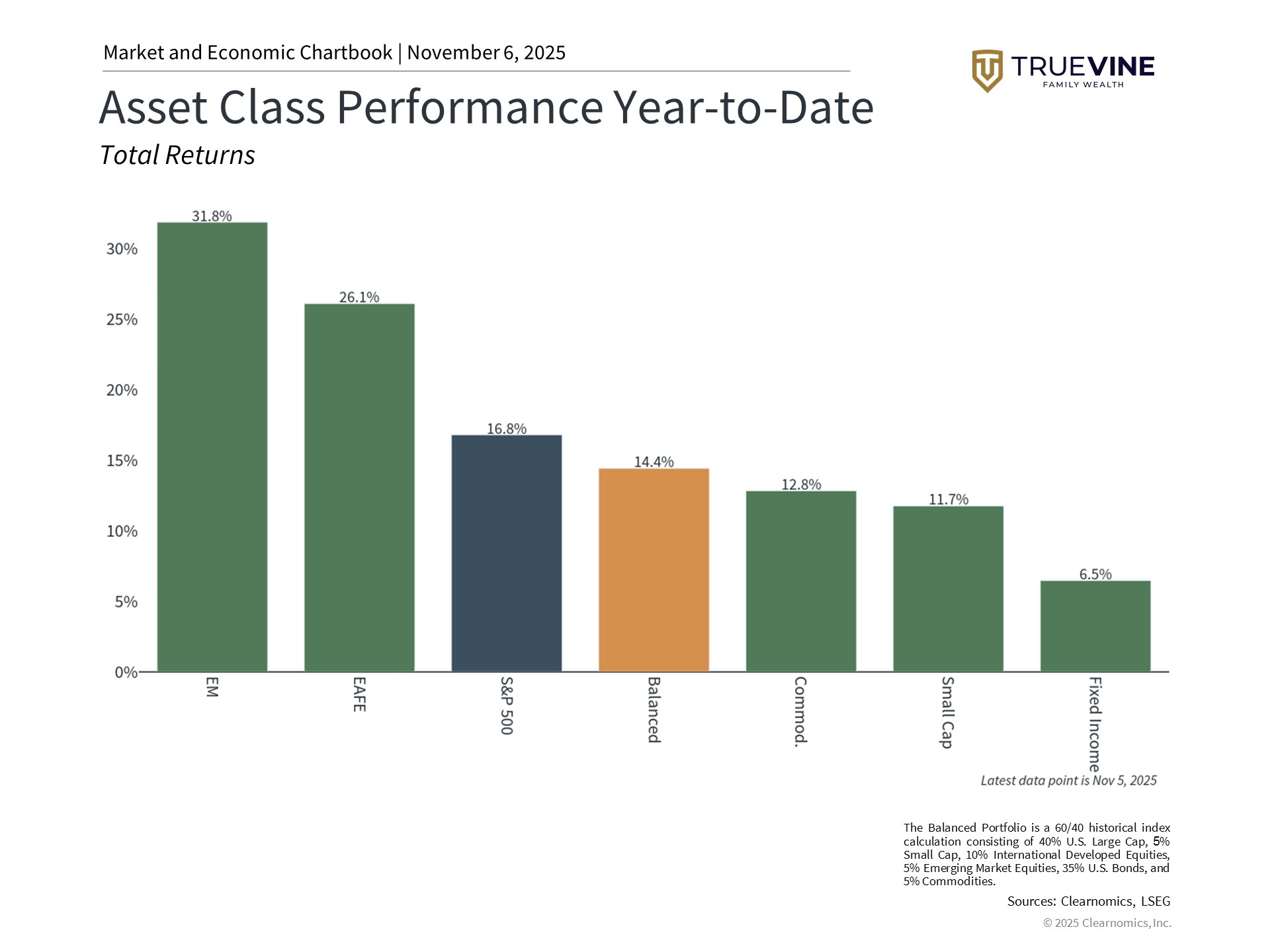

Multiple asset classes have driven portfolio gains this year

The current gold rally, which commenced in 2024, has coincided with robust performance across numerous assets, including artificial intelligence equities like the Magnificent 7, international stocks, fixed income securities, and cryptocurrencies. The accompanying chart demonstrates that diverse asset classes have contributed to portfolio returns this year. While gold has certainly delivered impressive results, individual securities and assets that excel in any given year will always exist.

For numerous investors, gold serves as one element within a broader commodities allocation, potentially alongside other alternative investments. The Bloomberg Commodity Index, for example, started the year with a 14.3% target allocation to gold. Combined with other commodities including silver, industrial metals, energy products, grains, and additional materials, this index has advanced 10.6% year-to-date.

Additional rationale exists for maintaining diversified holdings aligned with long-term financial objectives. A fundamental consideration is that gold produces no income stream, unlike fixed income securities or dividend-distributing equities. Therefore, portfolios excessively concentrated in gold forfeit the extended growth potential of stocks and the income generation of bonds.

This blog is published by TrueVine Family Wealth. The firm is registered as an investment adviser with the state of Florida and only conducts business in states where it is properly registered or is excluded from registration requirements. Registration is not an endorsement of the firm by securities regulators and does not mean the adviser has achieved a specific level of skill or ability. The firm is not engaged in the practice of law or accounting.

Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of any subjects discussed. All expressions of opinion reflect the judgment of the authors on the date of the post and are subject to change. Blog posts were prepared by Clearnomics, a third-party content provider.

You should consult with a professional advisor before implementing any strategies discussed. Content should not be viewed as an offer to buy or sell any of the securities mentioned or as legal or tax advice. You should always consult an attorney or tax professional regarding your specific legal or tax situation. Estate planning rules and regulations are subject to change at any time.

All investments have the potential for profit or loss. Different types of investments and strategies involve higher and lower levels of risk. There is no guarantee that a specific investment or strategy will be suitable or profitable for an investor’s portfolio. Asset allocation, rebalancing, and diversification will not necessarily improve a client’s returns and cannot eliminate the risk of investment losses.

Historical performance returns for investment indexes and/or categories, usually do not deduct transaction and/or custodial charges or an advisory fee, which would decrease historical performance results. There are no guarantees that an investor’s portfolio will match or outperform a specific benchmark. Historical returns do not represent the performance of TrueVine or any of its advisory clients.

Copyright (c) 2025 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.