The Federal Reserve and Politics: What Investors Should Know

Recent tensions between the White House and Federal Reserve have brought the topic of Fed independence into focus. This is because there can be a natural friction between elected officials and the Fed, since they each have unique goals and incentives.

For instance, the President and Congress often prefer lower interest rates to spur economic growth and help fund the federal budget. In contrast, the Fed may need to make difficult choices around issues such as inflation and financial stability, based on longer-term considerations.

The Fed is not without its critics, and there are countless history books detailing both the successes and failures of different Fed chairs. Still, Fed independence has been an important aspect of the financial system for decades. Today, much of the discussion on this topic centers around the legality of whether the President can fire a sitting Fed chair, the mechanics of what happens in that situation, and speculation over who would be nominated next.

However, what truly matters for investors is whether monetary policy remains appropriate and the economy remains stable. What do investors need to consider in the coming years regarding the Fed?

Fed Independence Has Evolved Throughout Its History

The chart above shows the nine Fed chairs appointed since 1948. Nearly all served under presidents of both parties, including re-nominations by other presidents. Jerome Powell, for instance, was originally nominated by President Trump in 2017, and was confirmed for a second term under President Biden. This chart also makes it clear that the economy has grown under different Fed chairs nominated by each party.

The concept of Fed independence is often taken for granted, so it’s helpful to briefly understand its history. As the country’s central bank, the Fed sets monetary policy and oversees the stability of the financial system. Independence means the Fed is free from political pressure, allowing it to make decisions based only on the economy and financial system.

This independence has developed over time. The Fed was not established by the Constitution, but rather by the Federal Reserve Act of 1913 passed by Congress. The Fed has a dual mandate which has also evolved over time, and is often interpreted as a) maintaining low unemployment, and b) an inflation target of 2%. Thus, the way monetary policy is conducted today is influenced by historical economic events including recessions and inflationary periods.

Following the Great Depression, the Banking Act of 1935 restructured the Fed, centralizing power within the Board of Governors and removing the Treasury Secretary from the Board to reduce political influence. During World War II, the Fed surrendered some independence by maintaining low interest rates to help finance the war effort. This continued until the 1951 Treasury-Fed Accord, which is widely regarded as re-establishing Fed independence by ending its obligation to support government bond prices.

The Inflation and Policy Environment Remains Complex

Perhaps the best parallel to today’s environment is the 1970s and early 1980s. Ahead of the 1972 election, President Nixon sought to ensure that easy monetary policy would support his campaign. Fed Chair Arthur Burns, who had been Nixon’s economic advisor, accommodated this by loosening monetary policy, which economists believe contributed to the inflationary pressures of the following decade.

- It wasn’t until the early 1980s, under Paul Volcker, that the Fed regained control of inflation by causing a recession. While most economists agree this is what ended the “stagflation” of that period, it came with political challenges. In his memoir, Volcker recounted pressure from the Reagan administration to not raise rates before an election.

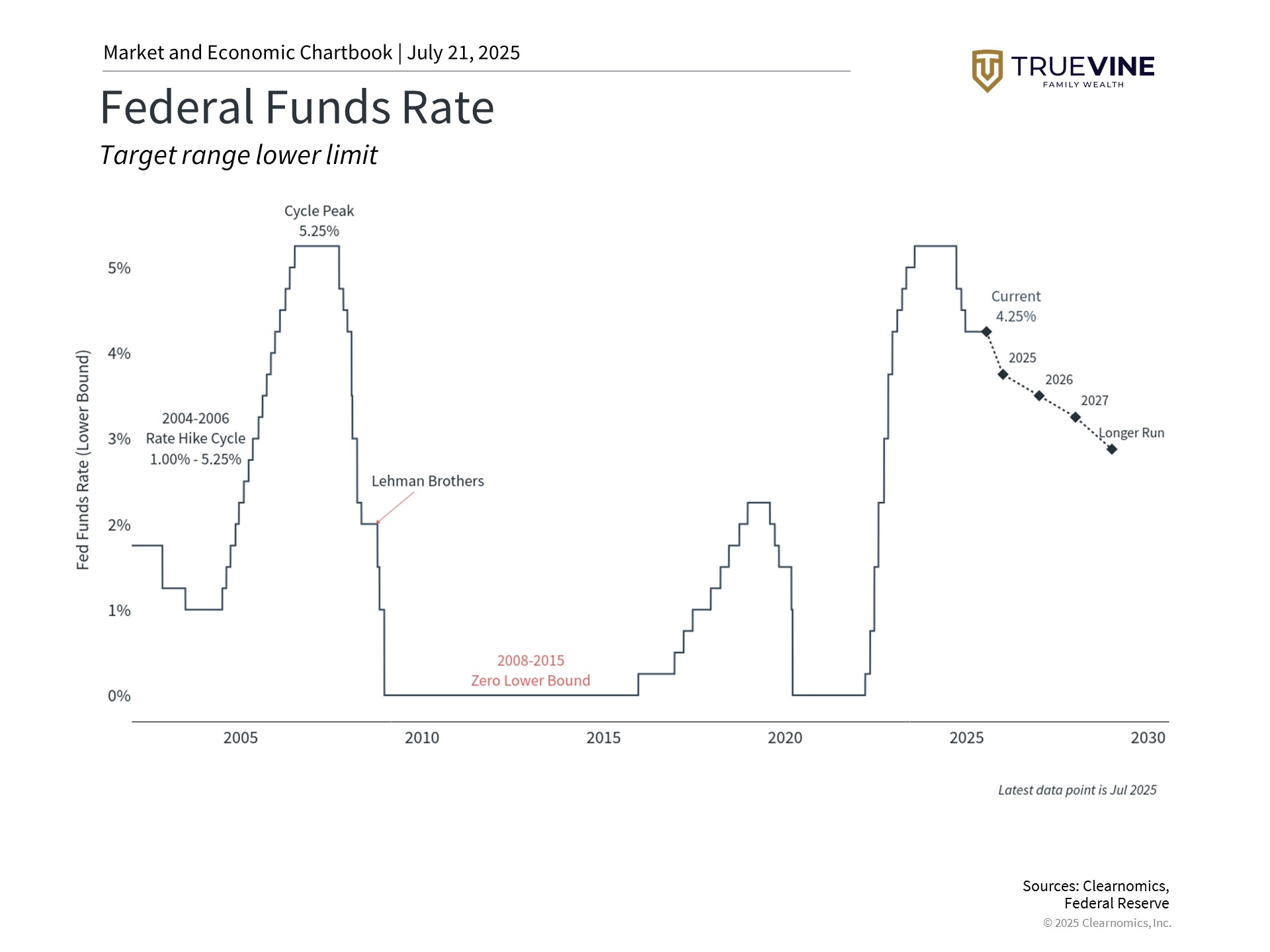

- In many ways, today’s economic environment echoes that of the 1970s since there are tensions between holding higher rates to ensure inflation improves, and lowering rates to spur growth. While inflation has been trending closer to the Fed’s 2% target, headline CPI remains at 2.7% and core inflation at 2.9% according to the latest report. Additionally, the Fed is taking a “wait-and-see” approach on whether tariffs will raise prices for consumers.

One way to understand this challenge is via the money supply, shown in the chart above. The money supply, which is managed by the Fed, typically increases steadily, supporting both stable growth and inflation. During crisis periods, such as in 2020, the money supply is used to support the economy. However, money supply growth has been flat in recent years as policymakers focused on combating inflation. Naturally, this can conflict with what some elected officials might prefer.

The Fed Is Still Expected to Cut Rates

Politics aside, the Fed is expected to cut rates further this year. It has been on hold following several cuts in late 2024 due to uncertainty around tariffs. The reality is that Fed policy exists to support long-term growth trends. When the economy is strengthening, the Fed’s job is to make sure it does not overheat – sometimes described as “taking the punch bowl away.” When the economy is weak, lower rates may be needed to jumpstart growth.

This balancing act is challenging, even in the best of times. In hindsight, the Fed is often accused of being “behind the curve.” For instance, Alan Greenspan, who served as Fed Chair for nearly 20 years, did not properly react to the housing bubble forming at the end of his tenure. More recently, some argue that the Fed raised rates too slowly in 2022 when there was already clear evidence of inflation.

What matters for investors and their portfolios is not to debate what the Fed should or should not have done. Instead, it’s to respond properly to the current investment environment with a long-term plan. History shows that changes in Fed leadership and shifts in policy can create uncertainty, but markets have performed well in spite of these challenges.

The bottom line? The market and economy have performed well under many different monetary policy and political environments. Maintaining a long-term plan that can navigate this uncertainty is still the best way to achieve financial goals.

- https://www.aeaweb.org/articles?id=10.1257/jep.20.4.177

- Volcker, P. A. (2018). Keeping At It: The Quest for Sound Money and Good Government

This blog is published by TrueVine Family Wealth. The firm is registered as an investment adviser with the state of Florida and only conducts business in states where it is properly registered or is excluded from registration requirements. Registration is not an endorsement of the firm by securities regulators and does not mean the adviser has achieved a specific level of skill or ability. The firm is not engaged in the practice of law or accounting.

Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of any subjects discussed. All expressions of opinion reflect the judgment of the authors on the date of the post and are subject to change. Blog posts were prepared by Clearnomics, a third-party content provider.

You should consult with a professional advisor before implementing any strategies discussed. Content should not be viewed as an offer to buy or sell any of the securities mentioned or as legal or tax advice. You should always consult an attorney or tax professional regarding your specific legal or tax situation. Estate planning rules and regulations are subject to change at any time.

All investments have the potential for profit or loss. Different types of investments and strategies involve higher and lower levels of risk. There is no guarantee that a specific investment or strategy will be suitable or profitable for an investor’s portfolio. Asset allocation, rebalancing, and diversification will not necessarily improve a client’s returns and cannot eliminate the risk of investment losses.

Historical performance returns for investment indexes and/or categories, usually do not deduct transaction and/or custodial charges or an advisory fee, which would decrease historical performance results. There are no guarantees that an investor’s portfolio will match or outperform a specific benchmark. Historical returns do not represent the performance of TrueVine or any of its advisory clients.

Copyright (c) 2025 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.