Understanding Social Security Adjustments and Strategic Portfolio Planning

Ensuring retirement savings can sustain a lengthy retirement remains the paramount concern for retirees and those nearing retirement. Inflation in recent years has significantly diminished the purchasing power of cash reserves, making this challenge more acute. Essential expenses that disproportionately affect retirees—such as healthcare, housing, and daily necessities—continue to reflect elevated price levels.

While equities and fixed income securities offer robust solutions to address this concern, risk aversion may lead some retirees to question whether their current holdings and savings can adequately counter rising living costs. For investors with extended time horizons, grasping how inflation impacts retirement income and determining optimal portfolio positioning to preserve purchasing power continues to be critically important. What essential insights should those in or planning for retirement understand about the current landscape?

As a Southwest Florida financial planner, I work closely with retirees and pre-retirees to develop personalized strategies that address inflation, income sustainability, and long-term wealth preservation. Every retirement plan should reflect your unique goals, risk tolerance, and lifestyle needs—not a one-size-fits-all approach. Partnering with a local advisor who understands both the financial landscape and the Southwest Florida market can make a difference in your legacy strategy.

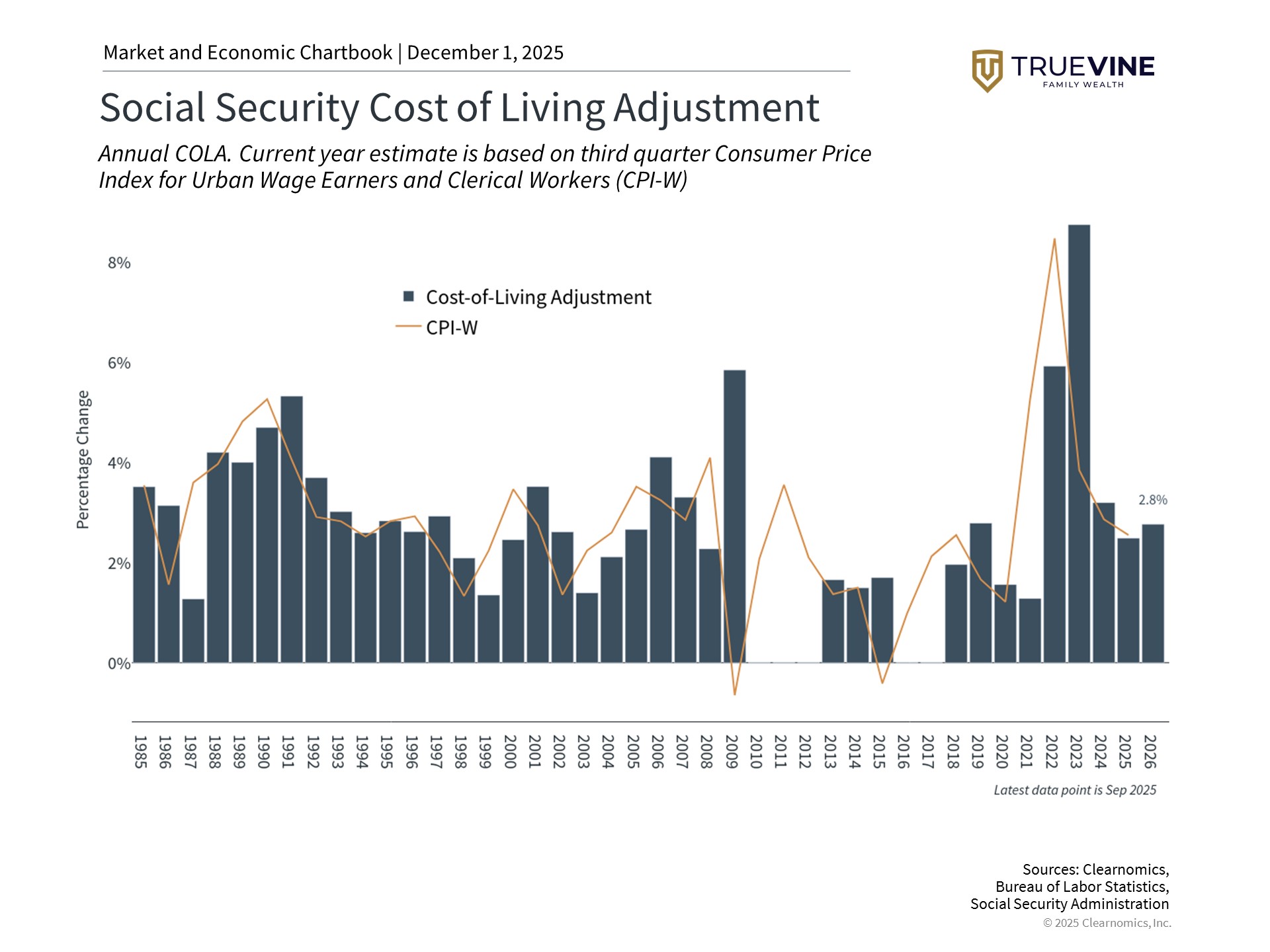

The gap between Social Security adjustments and actual inflation experienced by retirees

The Social Security Administration’s recent announcement of a 2.8% cost-of-living adjustment (COLA) for 2026 acknowledges ongoing inflationary pressures. Although any upward adjustment provides benefit, the inflation measurements used by economists often diverge from the price changes individuals encounter in their daily lives. This adjustment translates to an average monthly benefit of $2,064, representing a modest $56 increase—notably smaller than the 8.7% adjustment implemented in 2023, which marked the highest level since 1981.

A fundamental issue for those in retirement is that while the pace of price increases may decelerate, actual prices typically remain elevated rather than declining. The COLA calculation relies on the CPI-W, a Consumer Price Index variant that monitors prices for working-class households. This methodology fails to capture the reality that retirees frequently encounter inflation rates distinct from younger workers. Categories such as healthcare costs, housing expenditures, and other items that represent significant portions of retiree spending have frequently increased at rates exceeding those reflected in the broader index.

Consider these examples: medical care services experienced a 3.9% annual increase, health insurance rose 4.2%, and home insurance surged 7.5%. Food prices advanced 3.1% during this timeframe, though meat, poultry and fish specifically climbed 6.0%. Full service restaurant costs also became 4.2% more expensive.

Further complicating matters, Medicare Part B premiums may increase by $21.50 monthly in 2026, rising from $185 to $206.50 based on recent Medicare trustees’ projections. Because these premiums are generally deducted automatically from Social Security payments, this would consume roughly 38% of the average $56 COLA increase, further diminishing retirees’ actual purchasing power.

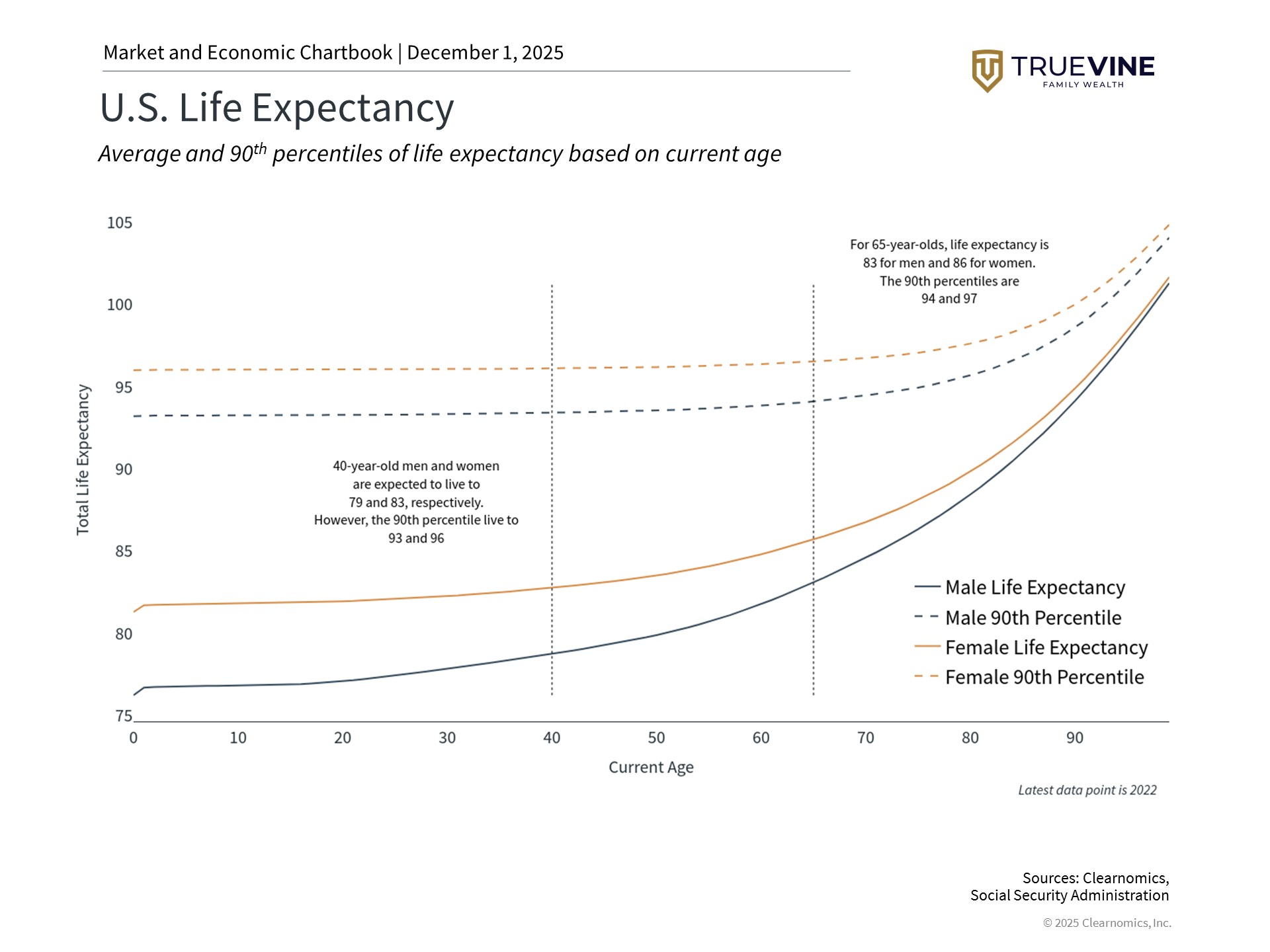

Extended longevity amplifies the necessity for portfolio appreciation

While investment gains can accumulate over extended periods, purchasing power erosion from inflation that outpaces portfolio returns similarly compounds. This consideration carries heightened significance today as retirees must account for potentially longer lifespans than prior generations. Consequently, life expectancy represents a crucial variable in comprehensive financial planning.

Based on current Social Security Administration statistics, 40-year-old males and females exhibit average life expectancies of 79 and 83 years, respectively. For individuals reaching age 65, these projections extend to 83 and 86 years. These figures represent averages—those in the 90th percentile may live to ages 94 and 97, respectively.

While the prospect of extended, healthier retirements represents remarkable progress over the previous century, the distinction between a 20-year retirement and one lasting 30 years or more carries profound implications for portfolio design and distribution strategies. This phenomenon, sometimes termed “longevity risk,” presents an asymmetric challenge since depleting assets during retirement creates far more severe consequences than bequeathing resources to beneficiaries or charitable organizations.

Therefore, although income-producing investments such as fixed income securities often receive priority in retirement planning, maintaining growth-focused assets like equities remains equally important. Extended lifespans also introduce financial complexities that elevate the value of sophisticated planning. Structuring portfolios for multi-decade retirement periods while managing distribution rates and adjusting to evolving market dynamics demands expertise that transcends conventional guidelines.

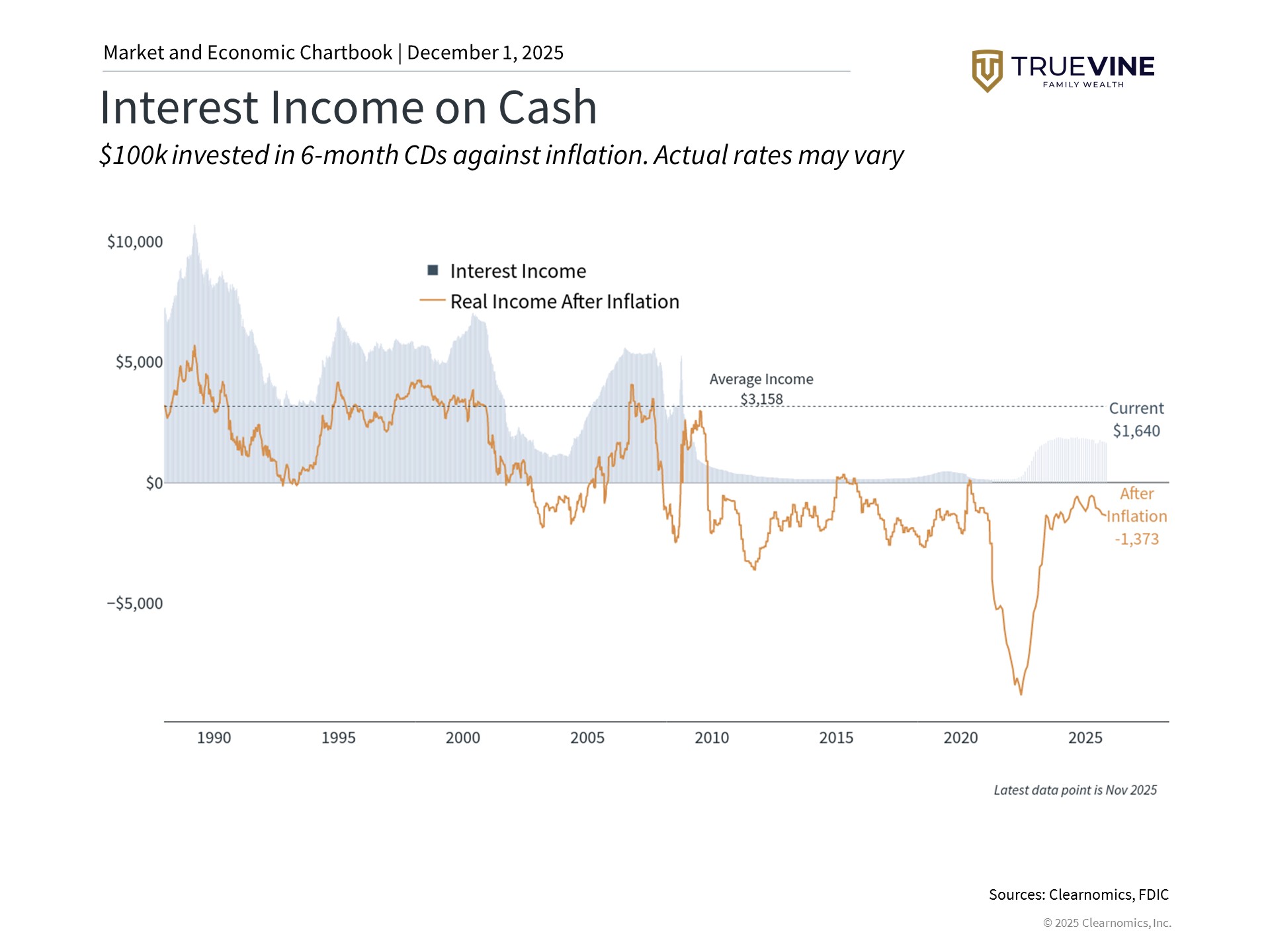

Declining short-term rates diminish returns on cash holdings

Recent Consumer Price Index information, released following delays from the government shutdown, carries implications for Federal Reserve policy and broader interest rate trends. With inflation moderating and employment markets softening, the Fed appears positioned to continue gradually reducing policy rates. While this transition benefits numerous economic sectors, it will likely diminish interest income available from cash holdings and money market accounts progressively.

For retirees who have relied on interest generated from cash positions in recent years, this transition toward lower interest rates may present difficulties. Although maintaining cash reserves for immediate expenses and contingencies remains prudent, excessive dependence on cash means forgoing the appreciation potential of equities and the compelling yields still accessible across various fixed income sectors.

The convergence of persistent yet moderating inflation with declining interest rates creates a demanding landscape for conservative investors. Cash holdings lose purchasing power to inflation while generating interest that will contract as the Fed pursues additional rate reductions. This dynamic underscores the heightened importance for retirees to maintain diversified portfolios encompassing growth-oriented assets like equities, which have historically exceeded inflation over extended timeframes, alongside fixed income securities that deliver income and stability.

The bottom line? Although Social Security COLA adjustments offer some protection against inflation, retirees cannot depend on these increases alone. Given increasing life expectancies and declining short-term interest rates, portfolios must be structured to deliver both income generation and capital appreciation.

This blog is published by TrueVine Family Wealth. The firm is registered as an investment adviser with the state of Florida and only conducts business in states where it is properly registered or is excluded from registration requirements. Registration is not an endorsement of the firm by securities regulators and does not mean the adviser has achieved a specific level of skill or ability. The firm is not engaged in the practice of law or accounting.

Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of any subjects discussed. All expressions of opinion reflect the judgment of the authors on the date of the post and are subject to change. Blog posts were prepared by Clearnomics, a third-party content provider.

You should consult with a professional advisor before implementing any strategies discussed. Content should not be viewed as an offer to buy or sell any of the securities mentioned or as legal or tax advice. You should always consult an attorney or tax professional regarding your specific legal or tax situation. Estate planning rules and regulations are subject to change at any time.

All investments have the potential for profit or loss. Different types of investments and strategies involve higher and lower levels of risk. There is no guarantee that a specific investment or strategy will be suitable or profitable for an investor’s portfolio. Asset allocation, rebalancing, and diversification will not necessarily improve a client’s returns and cannot eliminate the risk of investment losses.

Historical performance returns for investment indexes and/or categories, usually do not deduct transaction and/or custodial charges or an advisory fee, which would decrease historical performance results. There are no guarantees that an investor’s portfolio will match or outperform a specific benchmark. Historical returns do not represent the performance of TrueVine or any of its advisory clients.

Copyright (c) 2025 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.