How the Dollar, Gold, and International Stocks Fit Into Your Portfolio

Global events have been shaping financial markets, with geopolitics and new tariffs drawing a lot of investor attention. But one important factor that often gets overlooked is the value of the U.S. dollar. Currency movements can quietly affect your portfolio through their impact on international investments, commodities like gold, and the overall economy.

The dollar has declined from its 2022 peak but has bounced back somewhat recently, as investors tend to seek safety in dollar-denominated assets during uncertain times. Understanding what this means for other assets — like international stocks and gold — can help investors stay on track toward their financial goals.

Partnering with a Christian financial advisor can help investors evaluate how assets like the dollar, gold, and international stocks fit within a broader Christian financial planning framework. A TrueVine Family Wealth financial advisor in Naples, FL may offer perspective that emphasizes long-term strategy, diversification, and alignment with individual goals and values.

Three Things Investors Should Know About The Dollar

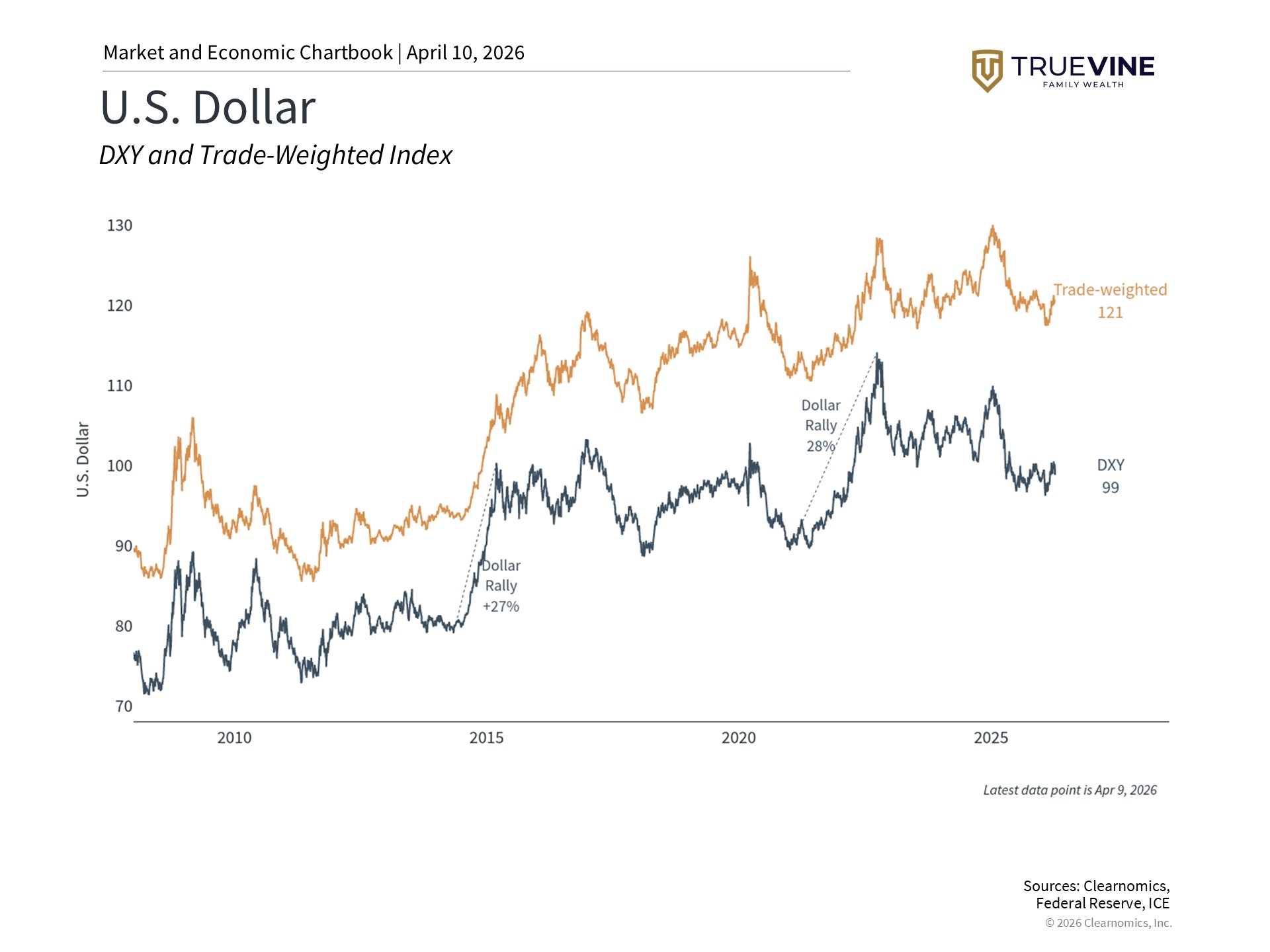

After peaking around 114 on the dollar index (DXY) in 2022, the dollar weakened as global growth stabilized. Tariffs pushed it below 100 for the first time in three years, though it has since partially recovered. Even with the decline, the dollar remains stronger than its long-term historical average.

Here are three key facts to keep in mind. First, a stronger dollar is not always a good thing. While it makes imported goods and overseas travel cheaper for consumers, it also makes U.S. products more expensive for foreign buyers, which can hurt American businesses competing globally.

Second, the dollar’s value is shaped by many factors, including interest rates, trade policy, and government spending. Interestingly, last year’s tariffs actually weakened the dollar rather than strengthening it — partly due to concerns that ongoing government budget deficits could erode the dollar’s economic standing over time.

Third, the dollar has rebounded since late January as geopolitical tensions have led investors back to safer assets. The dollar remains the world’s most widely used currency for international trade and reserves. While its dominance has been questioned before — during Japan’s rise in the 1980s, the introduction of the euro, and the growth of digital currencies — investors still tend to return to the dollar during difficult periods.

A Weaker Dollar Has Boosted Returns From International Stocks

The dollar’s decline over the past year has helped international stock returns. In 2025, developed market stocks (MSCI EAFE) returned 31.9% and emerging market stocks (MSCI EM) returned 34.4% in U.S. dollar terms — both ahead of the S&P 500. This highlights why diversifying globally can be valuable.

When a U.S. investor holds international stocks, those assets are priced in local currencies. If the dollar weakens, those foreign currencies convert back into more dollars, boosting returns. So currency movements add an extra layer to international investment performance.

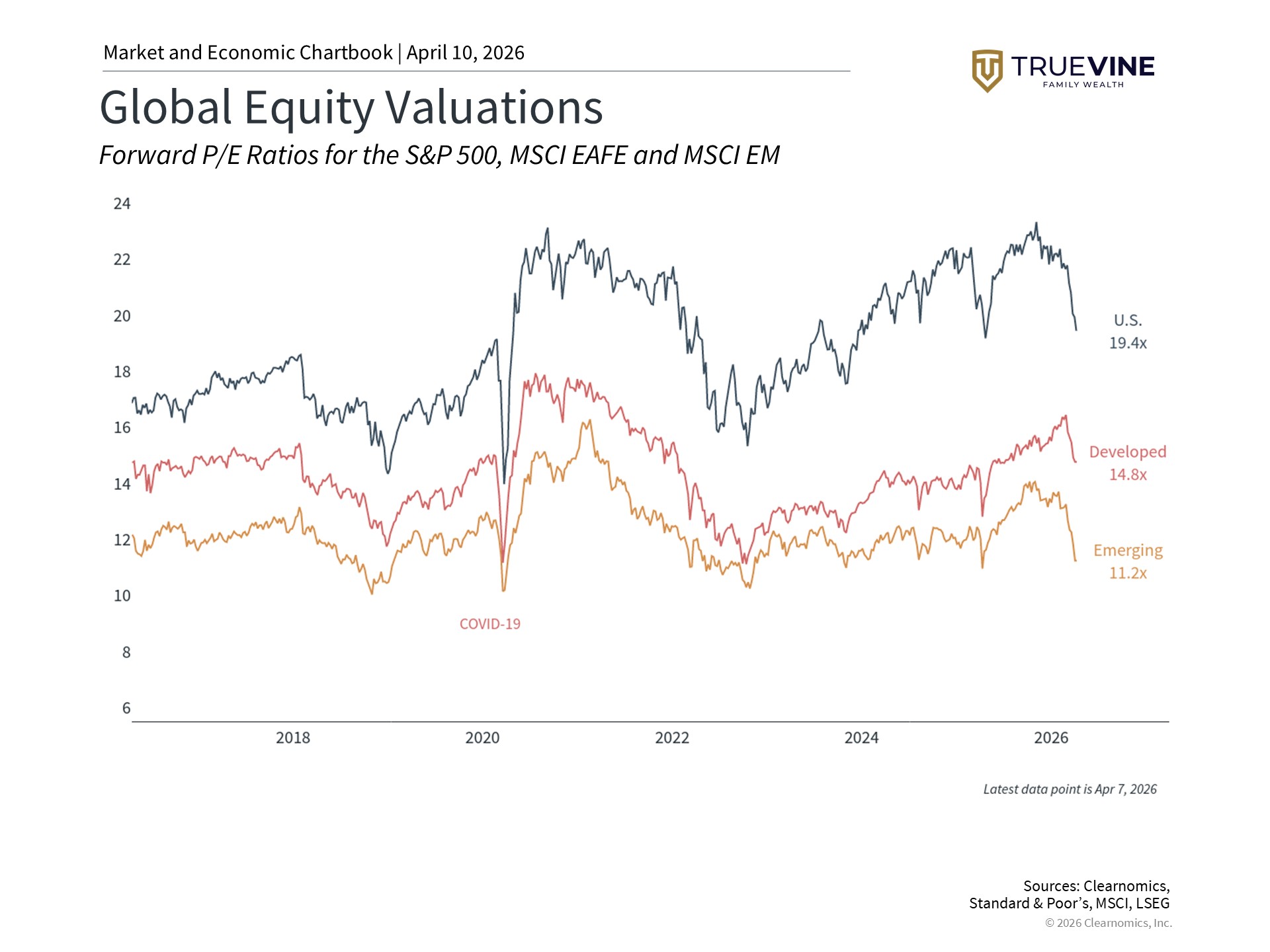

International stocks also look more affordable compared to U.S. stocks. Developed markets trade at a price-to-earnings ratio (a common measure of how expensive a stock is relative to its earnings) of 14.9x and emerging markets at 11.8x, compared to 19.9x for the S&P 500. While this doesn’t predict short-term returns, it’s a useful input when building a balanced portfolio. So far in 2026, international markets have continued to modestly outperform U.S. stocks, reinforcing the case for maintaining global diversification.

A TrueVine Family Wealth Southwest Florida financial planner who specializes in Christian financial planning can assist in assessing how different asset classes interact within a diversified portfolio. Working with a Christian financial advisor allows for thoughtful consideration of risk, time horizon, and overall investment objectives without overreacting to short-term market movements.

Gold Has Pulled Back After Reaching Record Highs

Gold has been widely discussed in recent years, driven higher by factors such as rising government deficits, lower interest rates, and geopolitical tensions. These forces pushed gold to an all-time high of $5,417 per ounce in late January. Since then, gold has declined roughly 14% from that peak, even though many of the same factors are still present.

Part of the reason is that gold had already attracted a lot of investor interest during its rally. When many investors pile into an asset expecting further gains, it can start moving more in line with other assets — meaning it may be sold during market stress rather than acting as a buffer. The dollar’s recent recovery has also weighed on gold prices, as the two often move in opposite directions.

This isn’t the first time gold has behaved unexpectedly. Between 2011 and 2020, gold was essentially flat despite low interest rates and periods of financial uncertainty. The most useful way to think about gold is as one piece of a broader, diversified portfolio — not as a standalone solution. Its value lies in the fact that it tends to behave differently than stocks and bonds, which can help smooth out portfolio performance over time.

This blog is published by TrueVine Family Wealth. The firm is registered as an investment adviser with the state of Florida and only conducts business in states where it is properly registered or is excluded from registration requirements. Registration is not an endorsement of the firm by securities regulators and does not mean the adviser has achieved a specific level of skill or ability. The firm is not engaged in the practice of law or accounting.

Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of any subjects discussed. All expressions of opinion reflect the judgment of the authors on the date of the post and are subject to change. Blog posts were prepared by Clearnomics, a third-party content provider.

You should consult with a professional advisor before implementing any strategies discussed. Content should not be viewed as an offer to buy or sell any of the securities mentioned or as legal or tax advice. You should always consult an attorney or tax professional regarding your specific legal or tax situation. Estate planning rules and regulations are subject to change at any time.

All investments have the potential for profit or loss. Different types of investments and strategies involve higher and lower levels of risk. There is no guarantee that a specific investment or strategy will be suitable or profitable for an investor’s portfolio. Asset allocation, rebalancing, and diversification will not necessarily improve a client’s returns and cannot eliminate the risk of investment losses.

Historical performance returns for investment indexes and/or categories, usually do not deduct transaction and/or custodial charges or an advisory fee, which would decrease historical performance results. There are no guarantees that an investor’s portfolio will match or outperform a specific benchmark. Historical returns do not represent the performance of TrueVine or any of its advisory clients.

Copyright (c) 2026 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.