Q2 2026 Market Update: What Geopolitics and Oil Prices Mean for Your Portfolio

The first quarter of 2026 is a good reminder of why preparation matters in investing. After strong gains in 2025, markets faced geopolitical shocks, rising oil prices, and fresh economic uncertainty. A conflict in Iran, which began in late February, became the biggest market story of the quarter, pushing oil prices sharply higher and triggering the first notable market decline of the year. By the end of March, talk of a possible ceasefire emerged, and the situation is still developing.

Looking at the bigger picture, markets have still performed well over the past twelve months. Energy and defensive sectors helped support portfolios during the turbulence. Looking ahead, a leadership change at the Federal Reserve and the midterm election later this year could bring new questions for investors.

Working with a Christian financial advisor in Southwest Florida can provide guidance in navigating market pullbacks with a long-term, stewardship-focused perspective. Rather than reacting to short-term volatility, investors can benefit from a disciplined approach that considers their overall financial plan, risk tolerance, and investment objectives.

Key Market and Economic Highlights

• The S&P 500 returned -4.3% in Q1, the Nasdaq -7.0%, and the Dow Jones Industrial Average -3.2%.

• The Bloomberg U.S. Aggregate Bond Index was flat for Q1 2026. The 10-year Treasury yield ended the quarter at 4.3%, down from a low of 3.9% in late February.

• International developed market stocks (MSCI EAFE) fell -1.1% and emerging market stocks (MSCI EM) declined -0.1%, both in U.S. dollar terms.

• Oil surged, with Brent crude reaching $118 per barrel at quarter-end, up from under $61 at the start of the year. WTI ended at $101 per barrel.

• Gold ended the quarter at $4,668 per ounce after reaching as high as $5,417 in January. The U.S. Dollar Index (DXY) edged up to 99.96.

• February inflation showed headline CPI up 2.4% year-over-year and core CPI up 2.5%. The Fed’s preferred inflation measure, core PCE, rose 3.1% year-over-year in January.

• The Federal Reserve held interest rates steady between 3.50% and 3.75% at both of its meetings in the quarter.

The First Market Pullback Of The Year

This year’s first quarter looks similar to early 2025 in some ways. Both periods saw S&P 500 pullbacks of exactly 4.3%. Last year’s volatility was driven by tariffs; this year’s was driven by conflict in the Middle East. In both cases, rising uncertainty caused short-term market swings.

History offers some perspective. Despite a rough start in 2025, stocks went on to post strong gains for the rest of the year, including dozens of new record highs. The point is not that markets always bounce back quickly, but that recoveries often happen when investors least expect them.

It’s also worth noting that pullbacks are a normal part of investing. Since 1980, the S&P 500 has seen an average decline of around 15% at some point each year — yet markets have finished higher in more than two-thirds of those years. Staying invested through short-term swings, especially those driven by news headlines, has historically been rewarded over time.

Geopolitics And Oil Prices Are Driving Uncertainty

The biggest market story this quarter was the escalating conflict in the Middle East, which sent oil prices sharply higher. Disruptions to the Strait of Hormuz — a key waterway that carries about 20% of the world’s oil supply — led to production cuts in the region. Brent crude ended the quarter at $118 per barrel, up over 94% year-to-date, while WTI surpassed $100 for the first time since the war in Ukraine began in 2022.

Higher oil prices lead to higher gas prices for consumers and raise costs for businesses throughout the economy. The national average for gasoline reached $4 per gallon at the end of March. That said, economists often view these kinds of energy price spikes as temporary, since oil prices tend to stabilize once a geopolitical situation settles. This was seen in 2022, when gas prices hit $5 before falling within months.

History also shows that geopolitical events, while unsettling, have rarely caused lasting damage to long-term investors. Investors who made big portfolio changes in response to past events often did so at the wrong time.

The Economy Is Slowing But Still Healthy

Beyond energy, the broader economy has cooled over the past year but remains in reasonably good shape. The labor market — one of the most closely watched areas — showed that February job gains fell by 92,000 and the unemployment rate edged up to 4.4%. For the first time in years, job seekers now outnumber available job openings.

Still, context matters. Fewer people are entering the workforce due to lower immigration and an aging population, which means both the supply and demand sides of the job market are cooling together. Consumer spending, which makes up more than two-thirds of GDP (gross domestic product — a broad measure of economic output), has remained stronger than many expected.

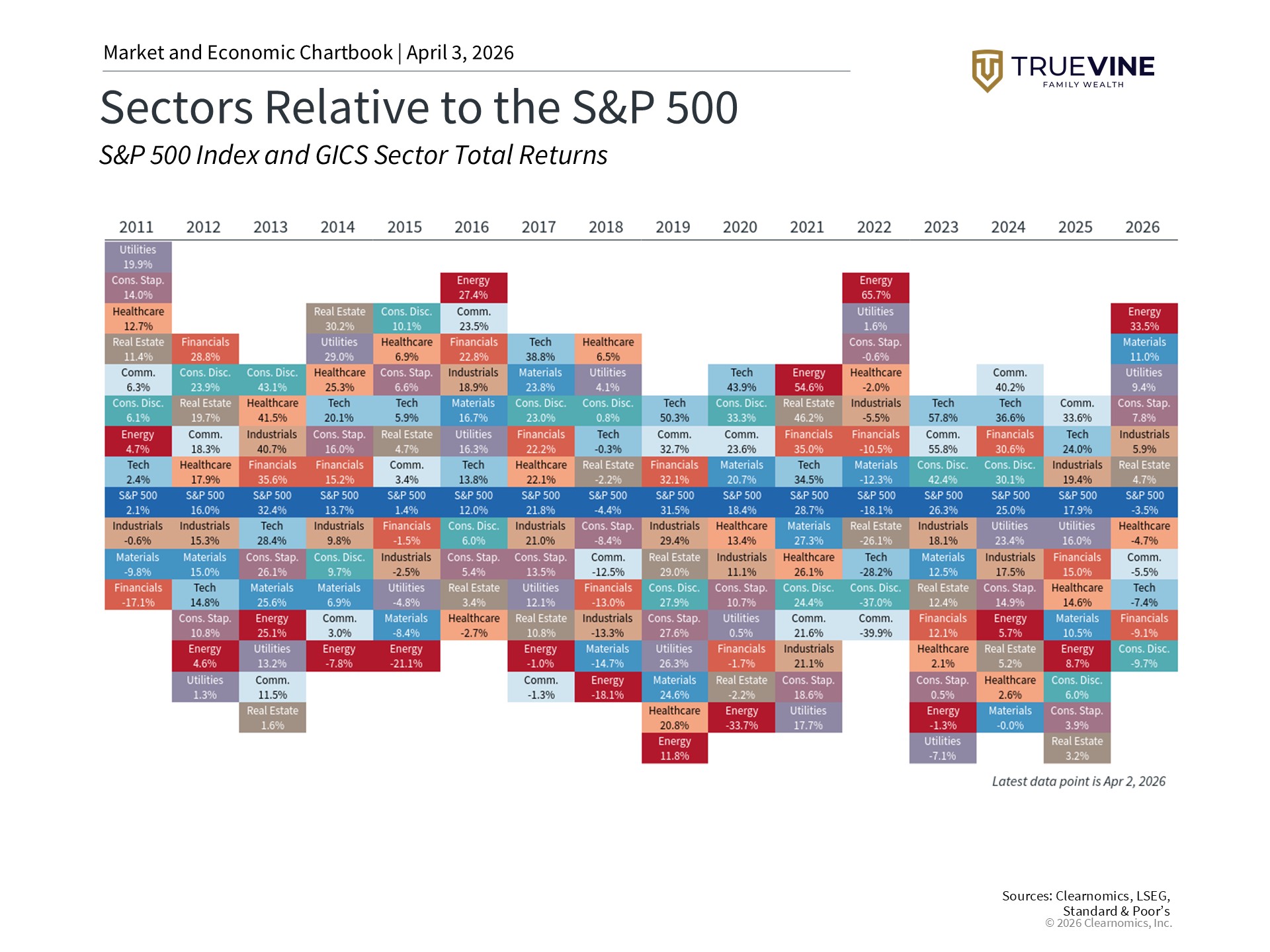

Some Sectors Are Outperforming While Others Lag

Not all parts of the stock market have moved in the same direction. Six of the eleven S&P 500 sectors are positive for the year, and the gap between the best and worst performing sectors reached nearly 50 percentage points in Q1. The Energy sector led the way, gaining nearly 40% through the end of March. Consumer Staples, Utilities, Materials, and Industrials also showed strength — these are often called “defensive” sectors because their businesses tend to be more stable regardless of economic conditions.

In contrast, the Information Technology sector fell about 9%, and many of the large technology stocks in the Magnificent 7 underperformed. This is a notable shift from recent years when a handful of large tech companies drove most of the market’s gains. Sector leadership changes regularly, which is why a diversified portfolio — one spread across different sectors and asset types — is better positioned to handle different market environments.

At TrueVine Family Wealth in Naples, FL, we take a holistic approach to planning and investment management by addressing the unique complexities of your business and personal life, ensuring they are mutually aligned to meet your overall strategic goals.

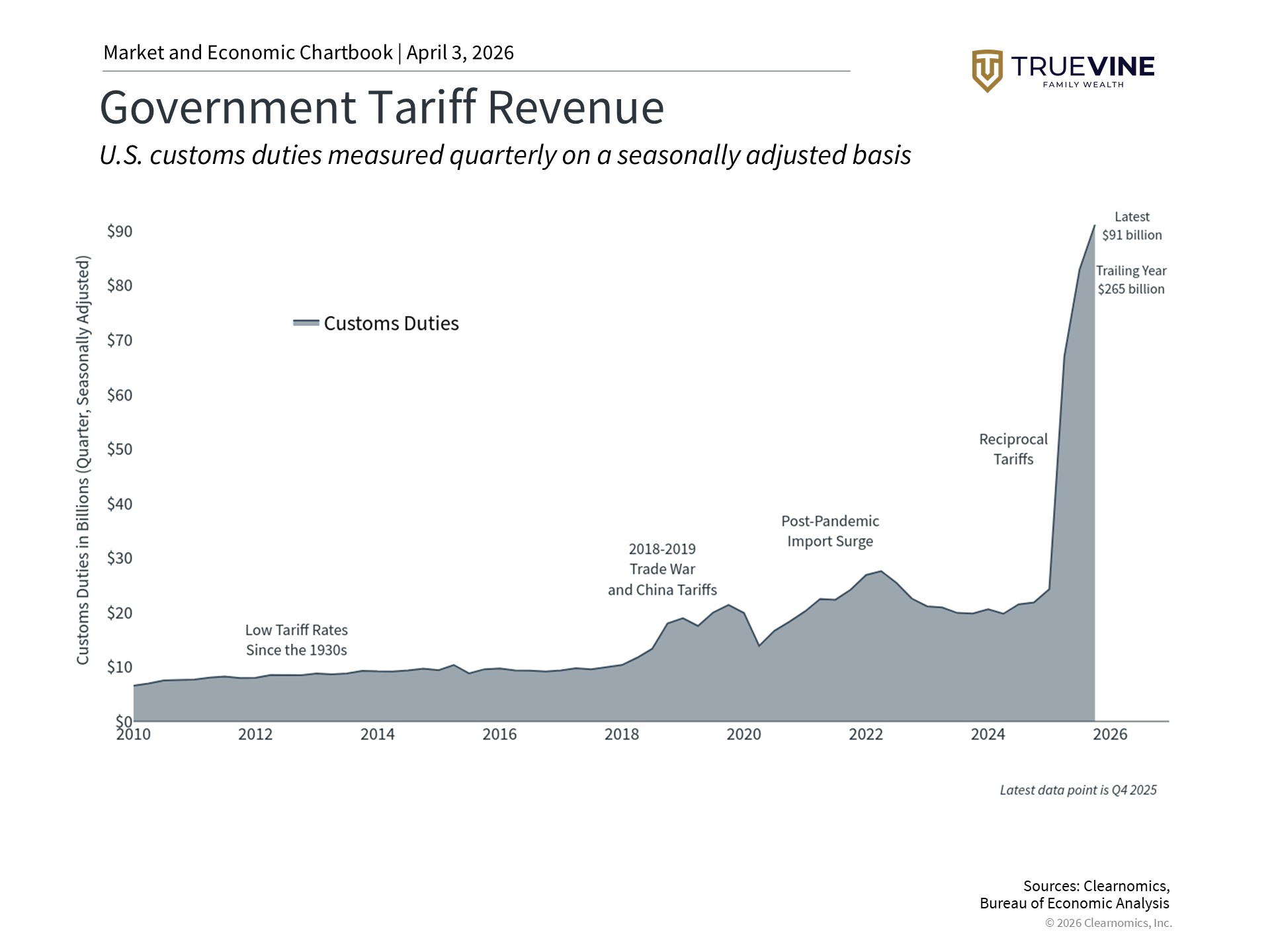

The Tariff Situation Continues To Evolve

Trade policy also shifted at the end of January after the Supreme Court ruled 6-3 that broad tariffs imposed under the International Emergency Economic Powers Act (IEEPA) were unlawful. The administration responded by imposing a temporary global import duty under a different law, Section 122 of the Trade Act of 1974, and opened new Section 301 trade investigations in March. About a dozen Section 232 investigations are also ongoing.

For investors, the key point is that while the legal approach to tariffs has changed, the broader direction of trade policy is likely to continue. Tariffs may affect consumer prices, business costs, and investor confidence. As 2025 showed, however, markets tend to adapt to policy changes over time. The best approach is to stay invested and avoid overreacting to policy headlines.

This blog is published by TrueVine Family Wealth. The firm is registered as an investment adviser with the state of Florida and only conducts business in states where it is properly registered or is excluded from registration requirements. Registration is not an endorsement of the firm by securities regulators and does not mean the adviser has achieved a specific level of skill or ability. The firm is not engaged in the practice of law or accounting.

Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of any subjects discussed. All expressions of opinion reflect the judgment of the authors on the date of the post and are subject to change. Blog posts were prepared by Clearnomics, a third-party content provider.

You should consult with a professional advisor before implementing any strategies discussed. Content should not be viewed as an offer to buy or sell any of the securities mentioned or as legal or tax advice. You should always consult an attorney or tax professional regarding your specific legal or tax situation. Estate planning rules and regulations are subject to change at any time.

All investments have the potential for profit or loss. Different types of investments and strategies involve higher and lower levels of risk. There is no guarantee that a specific investment or strategy will be suitable or profitable for an investor’s portfolio. Asset allocation, rebalancing, and diversification will not necessarily improve a client’s returns and cannot eliminate the risk of investment losses.

Historical performance returns for investment indexes and/or categories, usually do not deduct transaction and/or custodial charges or an advisory fee, which would decrease historical performance results. There are no guarantees that an investor’s portfolio will match or outperform a specific benchmark. Historical returns do not represent the performance of TrueVine or any of its advisory clients.

Copyright (c) 2026 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.